The Big Picture

|

- Our market letter will return in the New Year

| What Is The Purpose of QE?

Posted: 25 Dec 2012 02:00 PM PST As detailed earlier in the month, the Federal Reserve announced more stimulus, otherwise known as QE4, at its recent meeting. Lots of the discussion thus far has focused on whether or not QE will happen and not on the purpose of QE. What we discuss below is a good example of economists discussing the probability of QE rather than why QE is necessary or what it will accomplish. So, what is QE supposed to do? Bernanke told us in his speech over the summer in Jackson Hole: “After nearly four years of experience with large-scale asset purchases, a substantial body of empirical work on their effects has emerged. Generally, this research finds that the Federal Reserve’s large-scale purchases have significantly lowered long-term Treasury yields. For example, studies have found that the $1.7 trillion in purchases of Treasury and agency securities under the first LSAP program reduced the yield on 10-year Treasury securities by between 40 and 110 basis points. The $600 billion in Treasury purchases under the second LSAP program has been credited with lowering 10-year yields by an additional 15 to 45 basis points.12 Three studies considering the cumulative influence of all the Federal Reserve’s asset purchases, including those made under the MEP, found total effects between 80 and 120 basis points on the 10-year Treasury yield.13 These effects are economically meaningful. LSAPs also appear to have boosted stock prices, presumably both by lowering discount rates and by improving the economic outlook; it is probably not a coincidence that the sustained recovery in U.S. equity prices began in March 2009, shortly after the FOMC’s decision to greatly expand securities purchases. This effect is potentially important because stock values affect both consumption and investment decisions. While there is substantial evidence that the Federal Reserve’s asset purchases have lowered longer-term yields and eased broader financial conditions, obtaining precise estimates of the effects of these operations on the broader economy is inherently difficult, as the counterfactual–how the economy would have performed in the absence of the Federal Reserve’s actions–cannot be directly observed. If we are willing to take as a working assumption that the effects of easier financial conditions on the economy are similar to those observed historically, then econometric models can be used to estimate the effects of LSAPs on the economy. Model simulations conducted at the Federal Reserve generally find that the securities purchase programs have provided significant help for the economy. For example, a study using the Board’s FRB/US model of the economy found that, as of 2012, the first two rounds of LSAPs may have raised the level of output by almost 3 percent and increased private payroll employment by more than 2 million jobs, relative to what otherwise would have occurred.15 This is not the first time the Federal Reserve has laid out this argument. In a November 4, 2010 Washington Post op-ed, the day after QE2 was approved, Ben Bernanke defended their actions with the following passage:

Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending. Increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion. And in January 2011 Bernanke said:

Federal Reserve Board Chairman Ben Bernanke said Thursday that a controversial $600 billion bond buying plan has contributed to a stronger stock market. “Our policies have contributed to a stronger stock market just as they did in March 2009 when we did the first iteration of this program,” Bernanke said at a Federal Deposit Insurance Corp. forum on small businesses. “A stronger economy helps small businesses more than larger businesses. Interest rates are higher but that’s mostly because the news is better. It has responded to a stronger economy and better expectations.” To sum it all up:

We agree with half of what is written above.

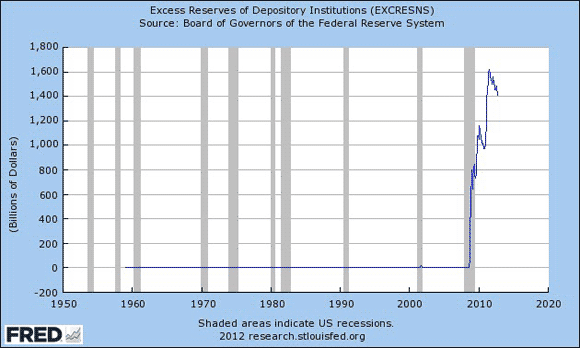

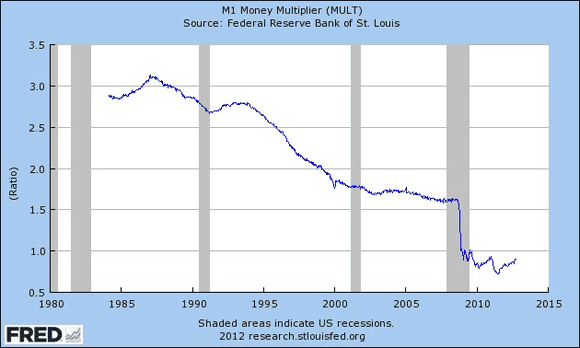

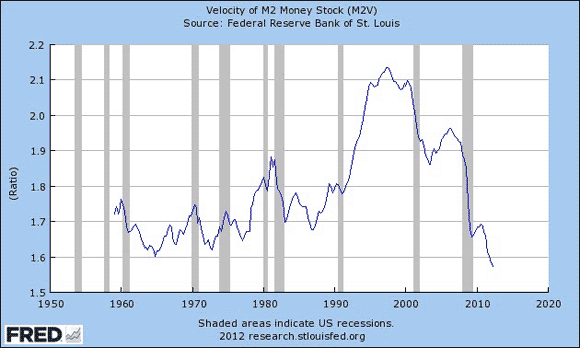

QE is great for Wall Street as it produces more volatility (brokers like this), higher stocks prices (fund managers like this) and draws lots of attention (analysts like this). It is not good for Main Street because it does not create wealth. QE’s effects are not perceived to be permanent, so it does not lead to higher GDP or job growth. What Will The Federal Reserve Do? In Septmber we noted that the median expectation in a survey of primary dealers calls for $500 billion of additional purchases heavily tilted toward mortgage-backed securities. If the purpose of QE is to push stock prices higher, then the Federal Reserve has to deliver at least $500 billion in purchases. Otherwise it will disappoint risk markets. Right now, if we have to guess, we believe the Federal Reserve will announce purchases of less than $500 billion. In January the Federal Reserve adopted an inflation target of 2.0%. As we detailed in a conference call last month (transcript, handout, audio), inflation expectations are running well above this target. One measure of inflation expectations, the 10-year TIPS inflation breakeven rate, is shown below. Further, in April, when Bernanke was asked if he would adopt a suggestion from Paul Krugman to expand the target to 3%, he flatly rejected the idea (explained here). The hawks will argue expected inflation is too high to add more stimulus, an argument which will carry some weight. The compromise will be a program of less than $500 billion in purchases which will disappoint the markets. Click to enlarge:

Source: Arbor Research

|

|

|

|

|

Related articles

- QE4 Is Here: Bernanke Delivers $85B-A-Month Until Unemployment Falls Below 6.5%. The US Must Go Down So The World Can Go Up!!! (tarpon.wordpress.com)

- Rumors of QE4 (amp2012.com)